Table Of Content

The result is the amount you can use in figuring your itemized deductions. Depending on your circumstances, you may need to figure your real estate tax deductions differently. Worksheet 2 is used to figure the adjusted basis of your home and your gain or (loss). You will figure your taxable gain (if any), on Worksheet 3, later.

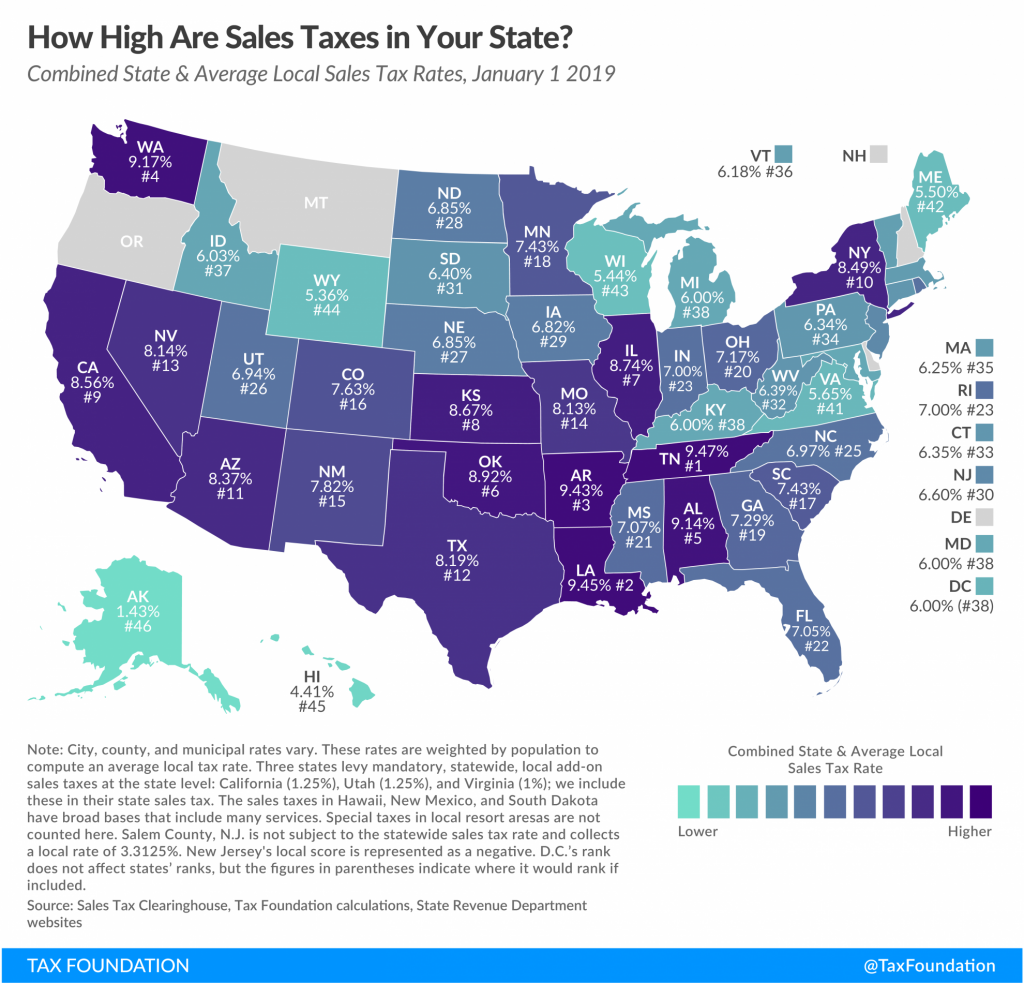

Transfer taxes exist too

Anyone who chooses not to claim the exclusion must report the taxable gain on their tax return. Taxpayers who receive Form 1099-S, Proceeds from Real Estate Transactions, must report the sale on their tax return even if they have no taxable gain. As we mentioned above, federal tax exemptions and taxes on home sales apply in California too.

Do You Pay Capital Gains If You Lose Money on a Home Sale?

The new basis for the interest your spouse owned will be its fair market value on the date of death (or alternate valuation date). Your new basis in the home is the total of these two amounts. If you or your spouse or ex-spouse lived in a community property state, see Pub. When you trade your home for a new one, you are treated as having sold your home and purchased a new one.

Offset Capital Gains With Capital Losses

You meet the ownership and use tests because you owned and lived in the home for 3½ years during this test period. Remember that, in any case, certain factors, such as any depreciation claimed for the home, may affect capital gains tax. It is also important to consider any state or local taxes that may apply to the sale of your home. If you don't meet the eligibility test for the maximum home sale exclusion, you may still qualify for a partial exclusion of gain.

Selling A House In Pennsylvania - Bankrate.com

Selling A House In Pennsylvania.

Posted: Thu, 01 Feb 2024 08:00:00 GMT [source]

What is capital gains tax on real estate?

They can provide personalized guidance based on your specific situation, help you understand tax implications, and ensure compliance with state and federal tax requirements. HomeLight makes it easy to find top-performing real estate agents in your market. We account for factors like the real estate agent’s sale-to-list price ratio and how that maps to local price trends so that you can find top agents who will put more cash in your wallet when you close.

These are the California cities where $150,000 still buys you a home. Could you live here?

If you or your family use the home for more than two weeks a year, it’s likely to be considered personal property, not investment property. This makes it subject to taxes on capital gains, as would any other asset other than your principal residence. If you inherit a home, the cost basis is the fair market value (FMV) of the property when the original owner died. For example, say you are bequeathed a house for which the original owner paid $50,000. The home was valued at $400,000 at the time of the original owner’s death.

A vacation home is real estate used recreationally and not considered the principal residence. Let's say you receive a job transfer and must sell your home 10 months after buying it. If you manage to sell it for more than you bought it for, you can reduce that profit by the amount it cost to acquire the home, plus any improvements you made that added value during the 10 months you were there. Depending on those two expenses, you may even avoid paying short-term gains. As a basic example, if you acquire a property for a $200,000 purchase price, pay $5,000 in acquisition expenses, and spend $20,000 to renovate the kitchen, your cost basis will be $225,000.

However, if your spouse or ex-spouse is a nonresident alien, then you likely will have a gain or loss from the transfer and the tests in this publication apply. In general, to qualify for the Section 121 exclusion, you must meet both the ownership test and the use test. You're eligible for the exclusion if you have owned and used your home as your main home for a period aggregating at least two years out of the five years prior to its date of sale. You can meet the ownership and use tests during different 2-year periods.

You cannot have bought the house through a like-kind exchange

However, personal residences do not qualify for 1031 exchanges for California or federal tax purposes. According to the Housing Assistance Tax Act of 2008, a rental property converted to a primary residence can only have the capital gains exclusion during the term when the property was used as a principal residence. The capital gains are allocated to the entire period of ownership. While serving as a rental property, the allocated portion falls under non-qualifying use and is not eligible for the exclusion. As a married couple filing jointly, they were able to exclude $500,000 of the capital gains, leaving $200,000 subject to capital gains tax.

For gains exceeding these thresholds, capital gains rates are applied. If you sell below-market to a relative or friend, the transaction may subject the recipient to taxes on the difference, which the IRS may consider a gift. Capital gains exclusions are attractive to many homeowners, so much so that they may try to maximize its use throughout their lifetime. Because gains on non-principal residences and rental properties do not have the same exclusions, people have sought ways to reduce their capital gains tax on the sale of their properties. One way to accomplish this is to convert a second home or rental property to a principal residence.

Determine whether any of the automatic disqualifications apply. For the latest information about developments related to Pub. 523, such as legislation enacted after it was published, go to IRS.gov/Pub523. Kiplinger is part of Future plc, an international media group and leading digital publisher. There are some simple steps to take that can help you prepare for what’s to come if you decide to sell a home in California. As the heir, however, you do take on any debts attached to the property, such as an outstanding mortgage.

Make the election by filing your tax return for the year of the sale or exchange of your main home, and exclude the gain from your taxable income. When you sell your house for more than you paid for it, you might have to pay capital gains tax. However, some situations may result in you paying very little or even nothing at all in taxes. If you are single and you lived in your house for two of the five years directly before the sale, the first $250,000 of any profit you make on the home is tax-free.

You add the cost of additions and improvements to the basis of your property. See Worksheet 2, later, for steps you should follow to figure your gain or loss. If an earlier home of yours was destroyed or condemned, you may be able to count your time there toward the ownership and residence test. Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more - straight to your e-mail. Get free, objective, performance-based recommendations for top real estate agents in your area. Max Efrein is a journalist who has covered a wide array of topics, including tracking real estate trends, for both traditional newspapers and online media.

No comments:

Post a Comment